Process Costing

Imagine a manufacturing company that specializes in producing one kind of products only but in mass units. The manufacturing costs in the company will be better understood as the raw materials move from one manufacturing process to the other. The manufacturing company could benefit from using process costing rather than job order costing.In process costing, the costs are allocated in each process of the manufacturing process. To use Process costing, the processes in a manufacturing plant must be identified and all the stages or departments of the manufacturing process noted. Then the costs of each department of the manufacturing process will be calculated and recorded as they are passed to the next process.

It is important to note that process costing and job order costing are some of the main costing accounting methods used in many manufacturing companies. Some companies may be using both costing methods while others use either of them. However, it is important to understand some of the main characteristics or differences between the job order costing and process costing methods.

| Process Costing | Job-Order Costing | |

|---|---|---|

| Products | Similar products Produced | Different products produced |

| Volume of Production | Mass production | Low volume |

| Production Process | Repetitive | Unique |

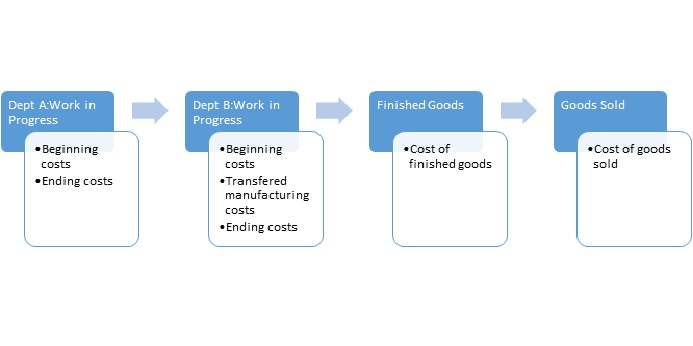

In progress costing all the jobs and their costs are identified and the flow of costs from one stage to another is recorded. The three main stages of the cost process include the work-in-progress, finished goods, and the cost of goods sold.

Every cost in the manufacturing process is accounted for as it moves from one stage to the other. If not all partial costs are transferred, the retained costs in a given stage are accumulated with the incoming costs.

An illustration of the flow of cost in process costing

The general flow of cost for process costing is;

←Back

←Back