Master Budgets

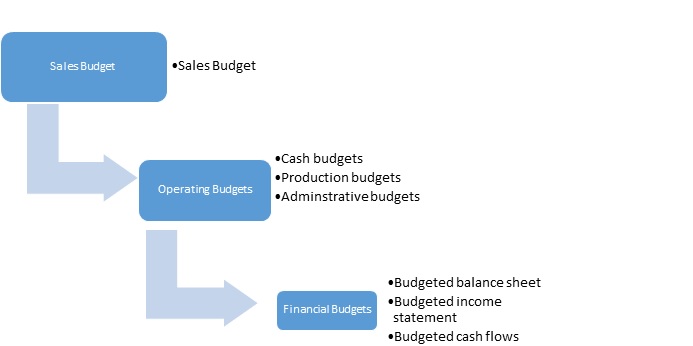

The main step of making a budget is making the master budget. Making a master budget starts with making a sales budget or a revenue budget. A master budget comprises of several individual budgets which together spells out an organization’s projection. The master budget consists of two main sections: operating budgets and financial budgets.The flow- chart of a master budget is as follows;

As noted, a master budget is made after the component budgets have been made or consulted by the appropriate managers. For example, when making the production budgets the production managers must be involved to understand the costs in each of the relevant departments of production, the sales manager must be involved in making the sales budget, etc.

It is important to note that the sales or revenue budget should be prepared first, followed by operating budgets before the financial budgets are prepared.

Since budgets are based on projections, it is important for managers to compare actual budgets with projected budgets. This comparison will enable the managers to better understand how to reduce costs to the required standards to maximize profits. The company’s actual financial statements such as the balance sheet, should be compared with the budgeted balance sheet to enable management understand the deviations in the budgets.